By Christmas Australia’s Aviation industry should be 60% back

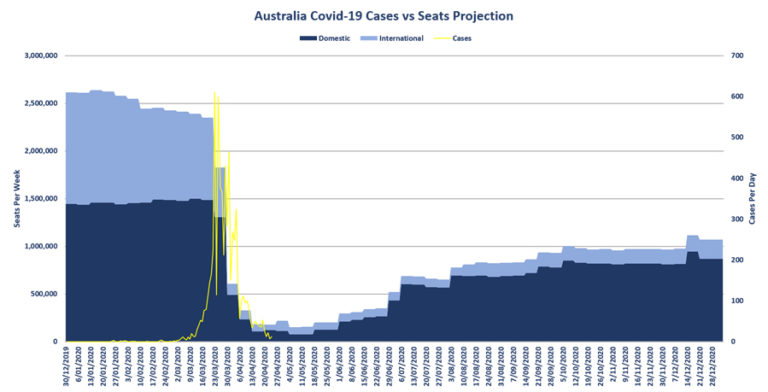

Based on a combination of analysis of government statements, airline projections, and underlying demand projects a slow, phased recovery in domestic air capacity in Australia through the remainder of 2020. Reaching 37% of last year’s volume by early July, Prime Minister Scott Morrison has foreshadowed a return to intra-state travel under the Federal Government’s three-phase plan to ease coronavirus restrictions. The plan, designed to revive the domestic economy, leaves the timing for the re-establishment of travel to the states. CAPA projects domestic capacity to reach 49% of 2019 levels by the October school holidays and 60% by mid-December 2020.

APA’s new ‘Airline Capacity Model’ has been developed to provide the aviation and travel industry with a robust guide to future air capacity possibilities anchored in:

- Actual baseline capacity data, drawn from OAG schedules and aircraft configuration data in the CAPA Fleet database;

- Decisions and announcements by the Prime Minister and State Premiers on travel restrictions and border announcements;

- Assessments by CAPA, based on real-time reports and unique daily news system which collects over 300 stories every day:

- Airline route plans and pricing;

- The public’s willingness and propensity to fly;

- The introduction of standard criteria on sanitary conditions onboard aircraft and at airports;

- ‘Right-sizing’ of aircraft to match demand.

- The airline capacity projections are updated in real-time, as major new events occur.

A supply-led return over the coming three months as airlines tempt passengers back to the air with low fares whilst emphasizing enhanced health and safety precautions. As demand rebuilds, supply (capacity and route network) will be adjusted to optimize yields and the market will steadily recover. CAPA will monitor industry updates and constantly update the Model.

Chairman Emeritus, Peter Harbison said:

“Australia is one of the best-positioned countries globally to suppress the first wave of COVID-19 infection. If this continues and we avoid a second outbreak, the Australian domestic air market could see some signs of life by mid-year and a steady improvement by Christmas. However, we don’t expect to see 2019 levels of domestic flying reached again this year. International will be hit harder and potentially take multiple years to recover. However, this will be to the benefit of the domestic market – potentially also embracing Trans Tasman operations”.

International markets are unlikely to recover and the CAPA Airline Capacity Model sees international air capacity (seat numbers) still down by 92% year-on-year in July, -86% in October, and -85% in December. The potential Trans Tasman ‘bubble’ with New Zealand has been factored into the CAPA Model from August, with some Pacific Islands linkages in time for the Christmas/New Year holidays.

The Model utilizes the following phased air capacity resumption scenarios. It is an interactive, excel-based model that allows users to then view the assumptions around the resumption of travel in domestic (state-based) and international markets, to build the overall capacity picture.

Capacity resumption phasing assumptions

| Phase | Name | Capacity (% of ‘Normal’ = 2019) | Description/Assumptions |

| 1 | Zero/Grounded | 0% | Travel bans resulting in the grounding of entire aircraft fleet |

| 2 | Skeleton | 5% | Airlines are providing a basic ‘skeletal’ network whether by its own volition or under some form of government/state subsidy, eg for:

|

| 3 | Commercial Resumption A – ‘Acutely Restricted’ | 25% | Airlines are resuming ‘Acutely Restricted’ commercial operations, to eg cater for:

|

| 4 | Commercial Resumption B – ‘Basic’ | 50% | Airlines are operating ‘Basic’ commercial operations, to eg cater for:

|

| 5 | Commercial Resumption C – ‘Constrained’ | 75% | Airlines are operating ‘Constrained’ commercial operations, to eg cater for:

|

| 6 | Commercial Resumption D – ‘Standard’ | 100% | Airlines are operating ‘Standard’ or normalised commercial operations, to eg cater for regularised:

|